Secured Loan vs Unsecured Loan: What’s the Difference and Which Fits Your Situation?

- Unsecured Loans

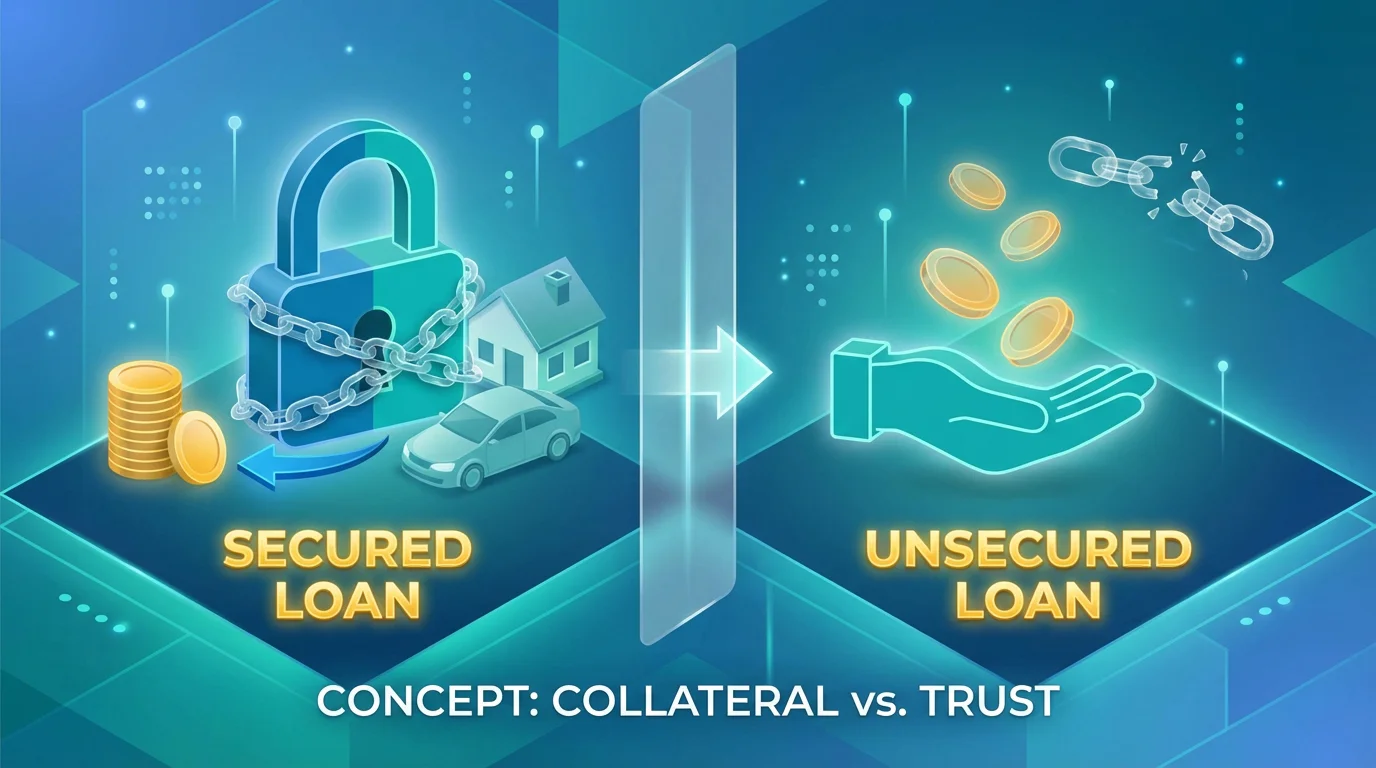

When comparing a secured loan vs unsecured loan, the biggest difference is simple: a secured loan requires collateral, while an unsecured loan does not. Collateral is property tied to the loan, such as a vehicle, savings account, or home. If the borrower defaults on a secured loan, the lender may have the right to take that asset. With an unsecured loan, there is no pledged property, but missed payments can still lead to credit damage, collections, and other consequences.

For many borrowers, the real question is not just which type of loan sounds better on paper. It is which one fits their situation, budget, and comfort level with risk. Some people focus on lower rates or larger loan amounts. Others care more about avoiding the risk of putting personal property on the line. That is why understanding the tradeoffs matters before applying.

Secured Loan vs Unsecured Loan: Quick Answer

A secured loan is backed by collateral. A lender takes on less risk because there is property attached to the debt. A classic example is an auto loan, where the vehicle helps secure the financing. An unsecured loan is not backed by collateral. Approval is usually based more on the borrower’s credit profile, income, and ability to repay. Because the lender has less protection, unsecured loans may carry higher rates in some cases.

The biggest risk with a secured loan is the possible loss of the asset. The biggest tradeoff with an unsecured loan is that it may cost more or require stronger approval factors. Neither option is automatically better in every situation. The right fit depends on what you need, what you qualify for, and how much risk you are willing to accept.

| Feature | Secured Loan | Unsecured Loan |

|---|---|---|

| Collateral required | Yes | No |

| Common examples | Auto loans, mortgages, some secured personal loans | Many personal loans, credit cards, student loans |

| Risk if payments are missed | Lender may repossess or foreclose on collateral | Credit damage, collections, possible legal action |

| Approval factors | Credit, income, and collateral value | Credit, income, and repayment ability |

| Possible rates | May be lower in some cases | May be higher in some cases |

| Loan amounts | May support larger amounts depending on collateral | May be more limited |

| Main borrower concern | Risk to property | Risk to credit and affordability |

What Is a Secured Loan?

A secured loan is a loan tied to something the borrower owns. That asset serves as collateral, which gives the lender added protection. If the borrower does not repay the loan as agreed, the lender may be able to take the collateral and sell it to recover some of the balance. Consumer guidance from the FTC explains this clearly with common examples such as car loans and mortgages, where default can lead to repossession or foreclosure.

Secured loans are often used for larger purchases or borrowing situations where the lender wants a stronger layer of protection. In some cases, that added protection can help support lower rates or larger loan amounts. That does not mean a secured loan is always the better choice. It means the lender’s risk is different, and that changes the structure of the deal. The borrower has to weigh that against the possibility of losing the pledged asset if repayment becomes a problem.

Examples of secured borrowing can include:

- auto loans

- mortgages

- home equity products

- some savings-secured or asset-backed loans

The key point is that the loan is not standing on the borrower’s promise alone. It is backed by property.

What Is an Unsecured Loan?

An unsecured loan does not require the borrower to pledge collateral. The lender is extending credit based mainly on the borrower’s financial profile, including factors such as income, credit history, and overall repayment ability. The FDIC explains that unsecured loans are made based on the borrower’s promise to repay and are not secured by collateral.

That makes unsecured loans appealing to borrowers who do not want to risk a vehicle, home, or other asset. Many common forms of consumer debt fall into this category, including most credit cards and many personal loans. CFPB materials also note that unsecured debt does not use property as collateral, but that does not mean there are no consequences if payments are missed. Lenders may still report negatively to credit bureaus, start collection activity, and in some cases sue to recover the amount owed.

For borrowers comparing options, this distinction matters. A loan without collateral may feel simpler and less risky at the property level, but it still creates a serious repayment obligation. It should still be evaluated carefully based on cost, monthly payment, and whether the amount borrowed actually fits the need.

Main Differences Between a Secured Loan and an Unsecured Loan

Collateral

Collateral is the clearest dividing line. A secured loan requires it. An unsecured loan does not. That one distinction shapes much of the rest of the comparison. When collateral is involved, the lender has another recovery path beyond normal collections. When there is no collateral, the lender is relying more directly on the borrower’s ability and willingness to repay.

Approval Requirements

Approval standards can differ because lender risk is different. A secured loan may sometimes be easier to qualify for when valuable collateral is involved, since the lender has added protection. An unsecured loan often depends more heavily on credit strength, income, and other signs of repayment ability. That does not mean secured loans are easy or unsecured loans are impossible. It means the lender is weighing risk differently.

Interest Rates and Total Cost

Secured loans may offer lower rates in some cases because the collateral reduces lender risk. Unsecured loans may cost more because the lender has less protection if the borrower defaults. The rate, however, is only part of the picture. Borrowers should look at the full cost of repayment, including the payment size, payoff timeline, fees where applicable, and whether the loan fits comfortably within the monthly budget.

Loan Amounts

Secured loans may support larger loan amounts, especially when the collateral has significant value. Unsecured loans may be more limited because there is no property securing the debt. This is one reason secured borrowing is often associated with large purchases or larger financing needs, while unsecured borrowing is often used for smaller personal expenses or shorter-term needs.

Borrower Risk

A secured loan can put specific property at risk. That is a major factor and should never be minimized. The FTC notes that secured debts tied to assets such as a vehicle or house can lead to repossession or foreclosure if payments stop. With unsecured debt, the borrower is not putting a specific asset on the line, but the consequences can still be serious. Credit damage, collections, and potential legal action are all possible.

Speed and Simplicity

Unsecured borrowing can sometimes feel simpler because there may be no collateral review, title issue, or asset valuation involved. That can make the process more straightforward in some lending situations. Still, borrowers should not assume any loan is automatically fast or easy. Approval and funding always depend on the lender’s process, the application details, and the borrower’s qualifications.

When a Secured Loan May Make Sense

A secured loan may make sense when the borrower is comfortable pledging an asset and understands the risks clearly. It may also fit situations where a larger loan amount is needed or where the structure of the loan is tied naturally to the item being financed, such as a vehicle or home.

In some cases, borrowers may find better pricing with a secured structure. That advantage has to be weighed carefully against the downside. If the payment becomes unmanageable, the borrower may be putting valuable property at risk. A lower rate is not enough reason by itself to choose a secured loan if the overall repayment picture is still too tight.

When an Unsecured Loan May Make More Sense

An unsecured loan may make more sense when the borrower does not want to pledge personal property or does not have an asset they are willing to use as collateral. This is often one of the main reasons borrowers prefer unsecured personal loans. They want to solve a short-term cash need, planned expense, or temporary gap without tying the debt to a car, house, or savings-backed account.

This option may also fit borrowers who want a more straightforward comparison based on monthly affordability, repayment terms, and total cost rather than collateral value. That does not make unsecured borrowing automatically safer. It simply changes the type of risk. Instead of risking a pledged asset, the borrower must focus on whether the payments truly fit the budget and whether the loan amount is necessary.

For many consumers, that distinction is the deciding factor. They would rather manage the loan through income and repayment planning than risk property they depend on.

Risks to Understand Before Choosing Either Option

Both secured and unsecured loans create a real repayment obligation. The fact that one does not require collateral does not make it casual debt. Borrowing more than needed, borrowing too quickly, or choosing a payment that strains the monthly budget can create problems either way.

With a secured loan, the risk to the asset is obvious. If the loan is tied to a vehicle or home, missed payments can create far-reaching consequences beyond the debt itself. With an unsecured loan, the consequences may look different, but they are still serious. CFPB materials note that unsecured lenders may use collections, furnish negative information to credit bureaus, and may sue in some cases.

A smart comparison should include these questions:

- Can I afford the payment without depending on best-case scenarios?

- Am I borrowing only what I need?

- Am I choosing this option because it truly fits, or just because it is available?

- If my income changes or an emergency comes up, what happens next?

The best loan is not simply the one you qualify for. It is the one you can repay realistically without creating a deeper financial problem.

How to Decide Between a Secured Loan and an Unsecured Loan

Start with the purpose of the loan. If the borrowing need is tied directly to a major purchase that naturally serves as collateral, a secured structure may be part of the normal decision process. If the goal is to cover a smaller expense without risking property, an unsecured option may feel more appropriate.

Then look at the risk. Are you comfortable putting an asset on the line? If the answer is no, that narrows the choice quickly.

Next, compare the full cost. Do not focus only on the monthly payment. Look at how long the debt lasts, what the total repayment may be, and whether the budget can handle it consistently.

Finally, think about consequences. A secured loan may bring property risk. An unsecured loan may bring credit and collection risk. Either way, the best decision is the one that matches the amount needed, the repayment plan, and the borrower’s real financial capacity.

Final Thoughts

The difference between a secured loan vs unsecured loan comes down to collateral, risk, and how the lender evaluates the loan. A secured loan may offer advantages in some cases, but it can put property at risk. An unsecured loan avoids that specific risk, but it still carries serious repayment consequences if the borrower falls behind.

Before choosing either one, compare the purpose of the loan, the total cost, the monthly payment, and the level of risk you are willing to take. A clear, careful decision is more valuable than rushing into the first option that looks available.

Key Takeaways: Secured Loan vs Unsecured Loan

- A secured loan requires collateral, while an unsecured loan does not.

- Secured loans may offer lower rates in some cases, but they can put your property at risk.

- Unsecured loans do not require collateral, but approval may depend more on credit, income, and repayment ability.

- Missing payments on either type of loan can lead to serious financial consequences.

- The better option depends on your budget, risk tolerance, and borrowing purpose.

Frequently Asked Questions

Is a personal loan secured or unsecured?

Many personal loans are unsecured, which means they do not require collateral. Some lenders may also offer secured versions, but unsecured personal loans are common in consumer lending.

Do unsecured loans always have higher interest rates?

Not always, but they may in many cases because the lender takes on more risk when no collateral backs the debt. The actual rate depends on the lender, the borrower’s profile, and the loan terms.

Can you lose property with an unsecured loan?

There is no pledged collateral in an unsecured loan, so the lender is not taking a specific asset at the outset. Still, missed payments can lead to credit damage, collections, and possible legal consequences.

Which is easier to qualify for: secured or unsecured?

It depends on the lender and the borrower’s situation. In some cases, secured loans may be easier to approve because collateral reduces lender risk. Unsecured loans may rely more heavily on credit, income, and repayment ability.

Which loan type is better for emergency expenses?

There is no one-size-fits-all answer. Some borrowers prefer unsecured borrowing for smaller urgent needs because they do not want to risk collateral. The better option depends on affordability, the amount needed, and the consequences tied to the structure.

Personal Loans From a Licensed Direct Lender

Take the Next Step with Galt Credit

If you’re comparing loan options and want a clear, simple way to apply, Galt Credit is here to help.

① Apply online in minutes with hassle-free process

② Review clear loan terms before you accept

③ Receive funds quickly as soon as the next day